That the U.S. dollar has strengthened over the past year should come as no surprise. Central banks in Japan, China, and the euro zone have loosened monetary policy via conventional and unconventional means, while the U.S. Federal Reserve appears poised to tighten monetary policy.

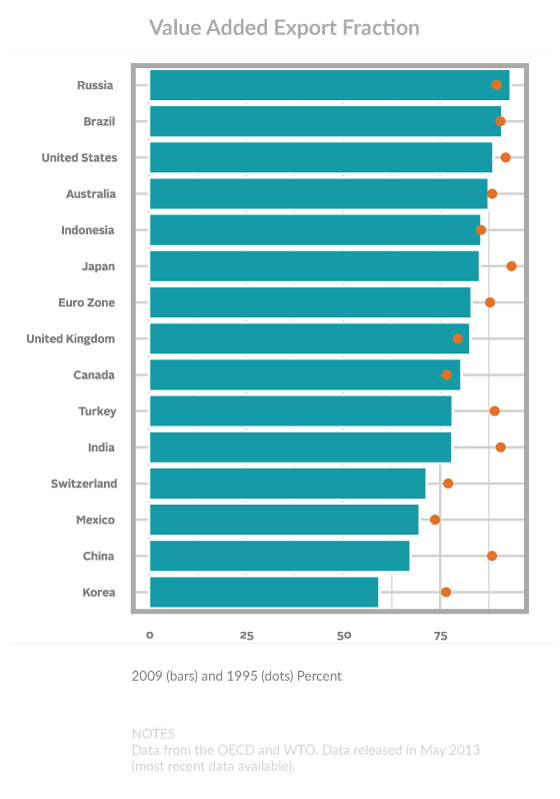

What may surprise some is that the exchange rate plays a 10–30 percent smaller role than it once did in international trade. As a result, the pain felt by U.S. exporters (and the drag on U.S. GDP growth) from the fourteen percent appreciation of the dollar since the beginning of 2014 should hurt the U.S. economy less than many might imagine.

Implications for investors

Two main implications arise from this analysis. The first and more direct implication is that the recent run-up in the dollar will less adversely affect U.S. exporters and GDP than would a similar run-up during a period (e.g., 1995) when a country’s domestic value add constituted a larger fraction of that country’s own exports. In other words, the “strong” dollar is not as bad as it looks for the U.S. or as good as it appears to exporters in Europe and Asia.

The second implication is subtler and less direct but no less important. The strength of the dollar relative to other currencies arises in part from central banks in Europe and Asia trying to spur domestic growth by loosening monetary policy. Part of those central banks’ calculus may include the hope that their weakening currencies will increase exports to regions enjoying relatively stronger growth (e.g., the U.S.), creating a self-reinforcing spiral of better domestic GDP growth. However, the declining amount of domestic value-add in their own regions’ exports suggests that the central banks efforts may prove less effective than they once were. These central banks may then need to increase their support in other ways.