By disentangling disagreement from uncertainty in polls of forecasters, asset allocators can draw a much clearer picture of what the data says and potentially hedge their exposures accordingly. For example, if half of polled experts believe with high conviction that one outcome appears likely, and the other half believe equally firmly that the opposite outcome appears likely, an asset allocator might want to hedge against two discrete scenarios. Alternatively, if all forecasters share a common expected outcome, but each feels highly uncertain of that outcome, an asset allocator might want to hedge against a broader range of scenarios.

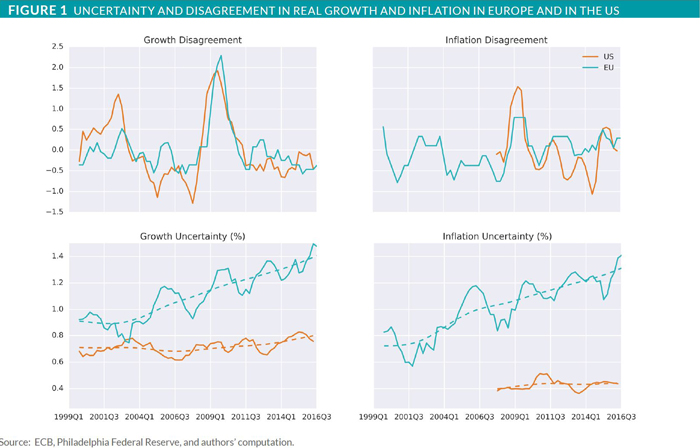

One can infer more than just the means from the surveys of professional forecasters by studying both the disagreement and the uncertainty of the forecasts. Consistent with academic research, disagreement equals the inter-quartile range (75th minus 25th percentile) of point forecasts, whereas uncertainty equals the average of the individual variances from each forecaster’s probability distribution of outcomes.1 Figure 1 depicts these two measures.

For GDP and inflation forecasts, data from the US Federal Reserve and the European Central Bank reveals two interesting findings. First, both US and European forecasters currently disagree with each other about as much as usual on growth and inflation. However, the level of uncertainty for each forecaster appears higher today than at any other time during the past 15 years, particularly in Europe. Asset allocators might want to incorporate that uncertainty when hedging their economic risk.