From a statistician’s perspective, some Generally Accepted Accounting Principles (GAAP) appear counterintuitive. For example, an illiquid asset like real estate may appear on a firm’s balance sheet with a value equal to the original price the firm paid, even for decades-old transactions. Such accounting rules seem to target precision (i.e., an observable but stale price) over accuracy (i.e., an unobservable “market” price).1 For a statistician craving unbiased data, these practices appear counterproductive.

These GAAP quirks notwithstanding, economists can actually make accountants look good in comparison. Consider GDP. To facilitate both intertemporal and cross-country comparisons, economists measure GDP as the market value of all goods and services produced within a country during a specified period. Complications to this measurement include both changes in market composition (e.g., unpaid household laborers joining the formal labor market and output like software applications given away for free) and changes in quality not reflected by price indices (e.g., improvements to video clarity that occur alongside declining television prices).

A different approach to measuring GDP growth

Economists often defend GDP as a useful metric using similar logic as accountants – an imperfect but sufficiently precise metric that offers more insights than most alternatives. So it seems only a little ironic that there exists a branch of macroeconomics called “growth accounting.”

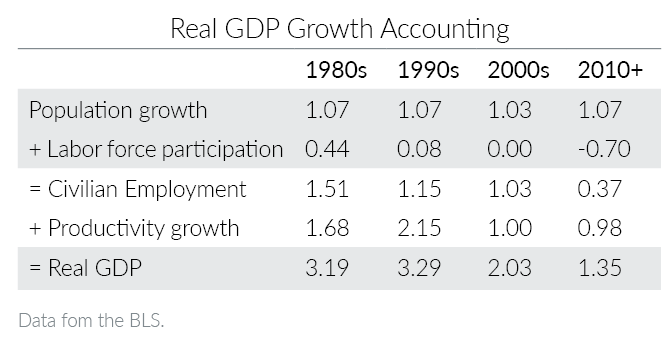

Growth accounting helps disentangle the drivers of GDP. For market participants and others striving to forecast US GDP growth rates, growth accounting can simplify the problem. Specifically, GDP growth equals the sum of the changes in labor productivity, labor force participation, and population growth. Along all three of these factors, the latest reports from the Bureau of Labor Statistics (BLS) provide disappointing news to anyone hoping that US GDP growth rates will return to the three percent per year (or higher) rate sustained prior to the Great Recession.