How will US GDP change during the next two years? For asset allocators evaluating the state of the global economy and pondering over its effect on asset prices, the question of the US outlook remains important. The answer, however, seems to have consistently eluded forecasters from many government, quasi-government (e.g., international authorities), and private organizations for the past five years.

Point-in-time forecasts from some of these organizations since 2011 show an interesting and statistically significant trend. During the past five years, forecasters have repeatedly proffered overly-optimistic predictions (by more than .50 basis points) for inflation-adjusted, long-term growth rates but excessively pessimistic predictions (approximately 25 basis points) for the near-term. As asset allocators begin planning for 2017 and beyond, they may want to account for this bias when formulating their own long-term outlooks.

IMF forecasts annual US GDP growth of 2.2 percent for 2017 and 2.1 percent for 2018, but the recent track record of its forecasts gives reason to doubt

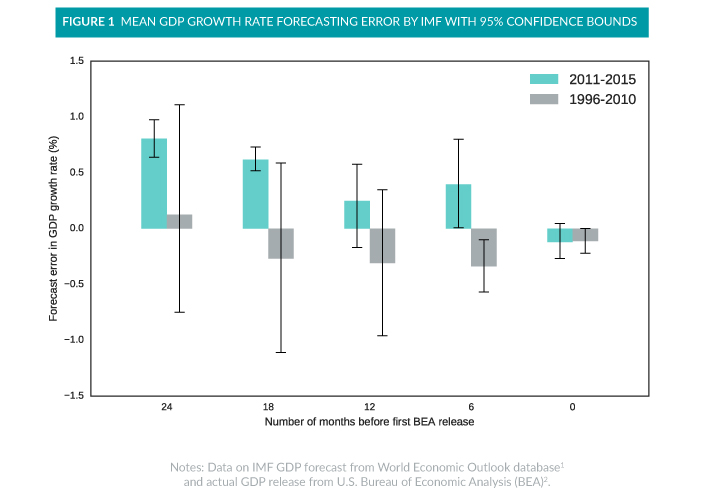

The forecasting history of the International Monetary Fund (IMF) offers a representative case study. The IMF releases analyses of global economic developments through its World Economic Outlook report, which is published twice per year. The IMF’s most recent forecast, from October 2016, predicts that the US economy will grow 2.2 percent next year and 2.1 percent during 2018. Historically, the IMF’s predictions have proven consistent with the subsequent official GDP estimate from the US Bureau of Economic Analysis (BEA). Figure 1 shows the mean ex ante forecast error with 95 percent confidence bounds for the IMF’s prediction relative to the BEA’s ex post report. The figure shows that the IMF’s forecast error did not differ significantly from zero between 1996 and 2010. This statistical result holds true for forecasts 24 months ahead and for forecasts less than six months ahead. However, since 2011, the IMF’s forecasts have exhibited a consistent bias. When making two-year horizon forecasts, the IMF has overestimated GDP by 50 to 100 basis points. The bias shrinks as the forecast horizon shortens.

Few other forecasters have proven more prescient during the past five years

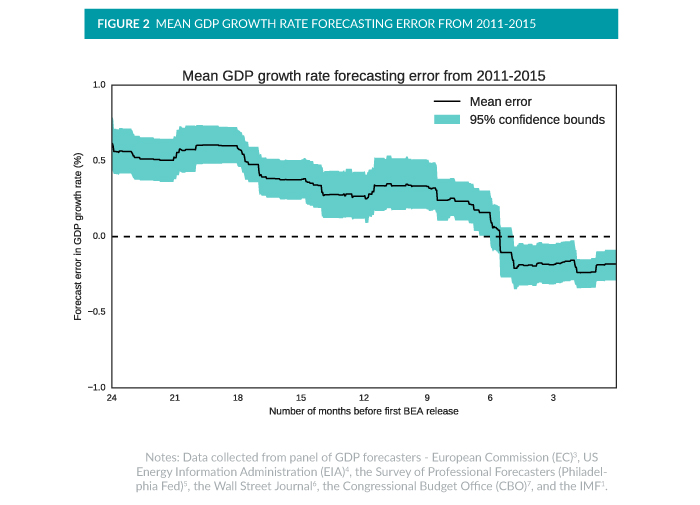

The IMF does not stand alone in offering too-rosy outlooks during the past five years. A closer look into US GDP forecasts since 2011 from a set of forecasters that also includes the European Commission (EC), US Energy Information Administration (EIA), the Survey of Profession Forecasters (Philadelphia Fed), the Wall Street Journal, and the Congressional Budget Office (CBO) reveals a similar upward bias.

Figure 2 shows the mean forecasting error in annual US GDP growth rate with 95% confidence bounds based on forecasts pooled across the full set during the most recent five-year period (2011-2015). Similar to the IMF, the average across all forecasters shows a positive bias (approximately 50 basis points) when looking two years ahead. The forecasts become more accurate as the forecast horizon shrinks, indicating that most forecasters tend to revise their estimates downward as data on actual economic conditions materialize. For near-term forecasts (i.e., less than six months), the average bias appears negative. In short, forecasters have been too optimistic about the long-term economic growth rate but too pessimistic about the near–term conditions.

Implications

Asset allocators planning for the next few years might still want to consider the views of experts from a range of government, quasi-government, and private institutions, but they would do well to remember that even these experts have struggled of late. In its latest annual real GDP forecast for the US (released in October), the IMF revised down its estimates for 2016 from 2.4 percent to 1.6 percent. Scientists rarely earn criticism for excessive optimism, but the data suggests that could change.