The year appears to be off to a reasonably positive start for equities globally, following a roughly 21% gain for the MSCI ACWI Index in 2017. Amid a generally favorable U.S. and European macroeconomic background, decent earnings growth, and realized volatility that’s approaching 50-year lows, market participants may find it tempting to be sanguine. But they should also be cognizant of important sources of potential “unconventional” risk—that is, risks that aren’t directly observable, particularly those of the monetary policy, political, and geopolitical varieties.¹

On the monetary policy front, the FOMC recently revised its growth projections higher and unemployment forecasts lower, and markets anticipate a series of three (or perhaps even four) rate hikes to come in 2018. Meanwhile, Fed officials appear to be keeping a close eye on inflation, and a new Federal Reserve chair is set to take office next month.

Political risks come in many forms, but most germane to publicly traded companies are those pertaining to fiscal policy (uncertainty around which has been rising, as we recently noted), regulatory changes, healthcare policy changes, infrastructure, and the like. And geopolitical risk remains a perennial concern, whether in the form of armed conflicts, trade disputes, or social unrest.

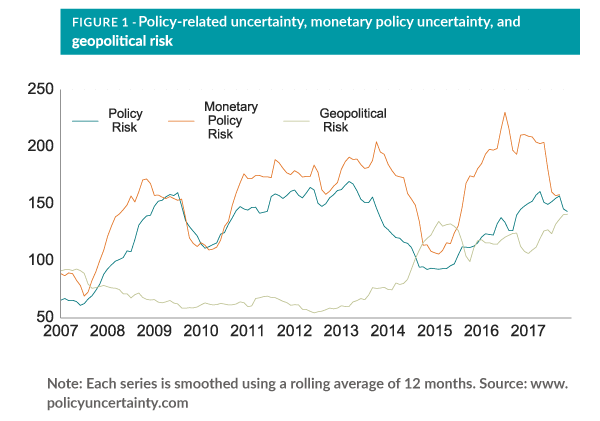

Measuring “unconventional” risk levels

The December 2017 issue of Street View described a method2 for estimating economic policy uncertainty following Baker, Bloom, and Davis (2016). Similar methods exist for measuring monetary policy uncertainty,³ firm-level political risk,⁴ and geopolitical risk.5 In summary, these methods parse broad corpora of texts (such as quarterly earnings conference-call transcripts and public news sources) to quantify into an index (displayed in Figures 1) language associated with the respective risks being measured.

As Figure 1 shows, monetary policy and firm-level political risk have been elevated since the aftermath of the global financial crisis, according to these proxies.6 While both have fluctuated over time and appear to be in a downtrend, they are nevertheless well above their post-crisis lows.

Geopolitical risk, on the other hand, appears to have remained subdued for years following the financial crisis before slowly beginning to climb in the wake of events such as the Arab Spring, the conflict between Russia and Ukraine, turmoil in Venezuela, Brazil, and Argentina, saber-rattling between the U.S. and North Korea, and others. Notably, unlike monetary policy uncertainty and political risk, geopolitical risk is near a 10-year high, with what may be little sign of abating.

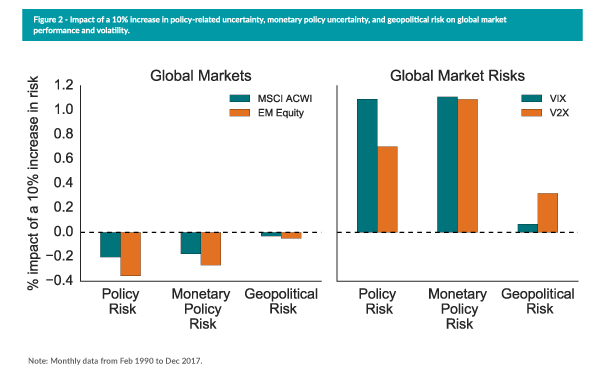

Do “unconventional” risks affect equity prices?

Although the political and monetary policy risk measures are U.S.-focused, their impact has the potential to affect global markets and volatility. Regressing the historical performance of global stock indices (MSCI ACWI Index and MSCI EM Index) and U.S. and European volatility indices against the risk factors may provide an idea of their market impact. As Figure 2 illustrates, each is negatively correlated with equity performance, with a larger impact on emerging market stocks. Their correlation with broad market volatility is positive, with increasing geopolitical risk having a greater impact on European volatility.

Implications for investors

If there is a silver lining to the notion that geopolitical risk is apparently rising, it may be that U.S. equities and the VIX have a history of mostly disregarding it (up to a point, at least). The same cannot quite be said for European volatility, however. And while the other “unconventional” risks appear elevated if not worsening, their impact—particularly on EM equities—has been more pronounced. It therefore would be wise for allocators to keep an eye on these risk levels as we move into 2018 and beyond