Quantifying political risk represents a hard problem for at least two reasons. First, political risk is usually unobservable. Direct measurements of the probability of a political event—e.g., the results of a referendum— prove exceedingly rare. Even when direct measurement exist, such as political prediction markets for US presidential elections, illiquidity reduces the information content of the implied risk forecasts.¹ Second, trying to quantify, or even identify the sign, on changes in political risk often requires subjective interpretation.

Many asset allocators still need to address this hard problem, because important political challenges await financial markets in 2017, all of which could increase market risk and significantly undermine investors’ asset allocation. These include the coming presidential elections in France, the federal elections in Germany, the ongoing parliamentary debate in the UK on how to trigger Brexit, and prevailing post-referendum political instability in Italy.

Fortunately, academic research such as Rigobon (2003) offers a simple, tractable approach to try to empirically model the effects of political risk on financial markets. The Italian referendum on December 4 offers one case study, but asset allocators might also find the approach insightful for other upcoming events during a potentially politically tumultuous 2017.

One approach to measuring the effect of political risk

An approach to quantifying the effect of political risk on financial markets should have a few characteristics, at least from the perspective of many data-driven practitioners. First, it should prove empirically practical in a world relatively abundant in political news but sparse in publicly available political data. Second, the approach should require little subjective interpretation, because even the best interpreters struggle with political linguistics. Third, it should feel relatively intuitive.

Rigobon (2003) offers one such approach in applications ranging from Latin American sovereign bonds, to the second US-Iraq war, and to the US Federal Reserve’s monetary policy.2 The methodology compares the volatility of financial variables on days of discrete political events, such as elections or prime minister’s resignations, to the volatility on other days. Analyzing the second moment (i.e., volatility) of the asset return distribution instead of the first moment (i.e. mean) makes the hard problem of political risk analysis much easier. According to the Rigobon (2003) approach, researchers (and asset allocators) need only define when political news took place rather than trying to quantify the magnitude and direction of that news.

Practically, this means taking the following steps (according to Rigobon 2003):

Step 1: Define the treatment group, or a set of “event” days on which the variance of the unobservable factor is high, such as the Italian referendum on December 4.

Step 2: Choose a set of “non-event” days to serve as a control or comparison group. Common practice suggests choosing non-event days one or a few days before the event days, so as to minimize the influence of risk factors other than the political one. Political risk may also change on these days, but (by assumption) they change less than on event days. This assumption is a leap of faith, but hopefully a reasonable one.

Step 3: Apply a standard econometric technique known as instrumental variable (IV) regression. Consider regressing changes in one variable of interest (e.g., the CDS spread of Spanish sovereign debt) on changes in a second variable (e.g., Italian CDS spreads), that is then instrumented by a proxy.3 This proxy is the same variable but with opposite sign on non-event days.

Unlike a traditional event study, this approach does not apply the unrealistic assumption that political risk only changes on event-days. In situations like the Italian referendum, in which periodic polls revealed changes in voter preferences, the traditional event-study method may underestimate the magnitude of the political risk.

Case study: the financial market consequences of increasing political risk in Italy

The Italian constitutional referendum, held on December 4, triggered a heated debate on the possible consequences for local and broader European markets. Most of this debate stemmed from fears over the resignation of Prime Minister Matteo Renzi, who vowed to resign in the event of a “no” vote. Over the past decade, some prime ministers’ resignations from the Italian government seem to have caused meaningful declines in European equity markets. For example, in the autumns of 2011 and 2012, when first Silvio Berlusconi and then Mario Monti resigned, financial markets throughout Europe slumped significantly.4 The equity market response this year proved more muted, perhaps because the outcome of the referendum was less surprising.

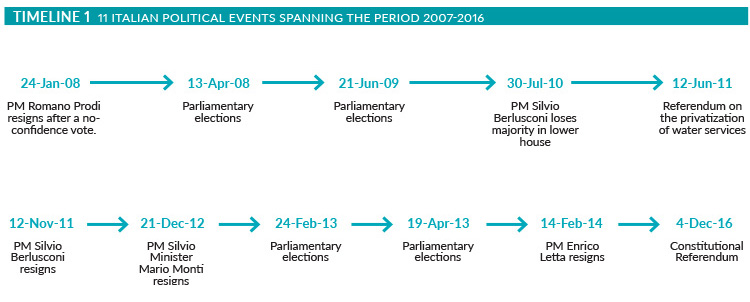

One way of quantifying the impact of the Italian political risk factor on the credit risk of European economies is by using a set of eleven political days listed in Timeline 1. These include: i) four prime minister resignations (Jan-08, Nov-11, Dec-12, Feb-14); ii) four parliamentary elections (Apr-08, Jun-09, Feb- and Mar-13); iii) two referendums (Jun-11, Dec-16); and iv) a no-confidence vote in which the then governing party lost its majority in the lower house (Jul-10). (See Appendix for details.)

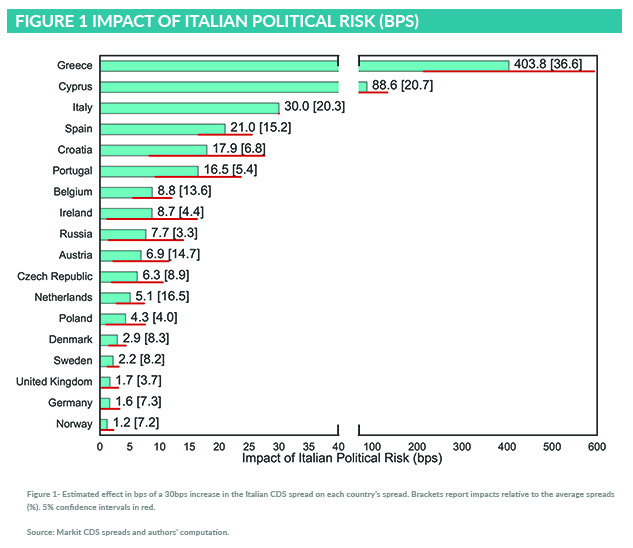

In particular, using the 5-year Italian credit default swap (CDS) spread and that of a set of 34 countries worldwide, Figure 1 plots statistically significant potential impacts on the credit spread of other countries from a political shock in Italy that increased the Italian credit spread by 30 basis points.5

The figure shows that political events in Italy have the potential to spill over to other countries. Political shocks hit Greece and Cyprus heavily, with increases in credit risk of about 404 and 89 basis points, respectively, accounting for about 37 and 21 percent of the average spread, respectively (number in brackets). Spain is next in line with a spread increase of 21 bps, roughly as high as that of Italy, representing a relative change of 15 percent. Political events in Italy also mattered for Portugal, Belgium, and Ireland, countries that appear to share certain similar characteristic with Italy, such as prolonged political instability (in the case of Belgium), and large indebtedness relative to the size of the economy (Portugal and Ireland). Additionally, the impact on Germany, the UK, and Norway was lower (about 1.5 bps) but still appear statistically significant.

Potential implications

The idea that an unobservable risk factor may have material spillover impacts on financial markets might not surprise asset allocators. However, the non-observability of political risk makes it challenging for allocators to quantify the associated effect using traditional approaches. The approach outlined in Rigobon (2003) provides a solution to measuring the impact of unobservable risk factors.

In the face of numerous political significant events in 2017, particularly in Europe, allocators might consider using this technique to potentially stress-test their portfolios. The hard work of trying to figure out which events might matter lays ahead. Fortunately, academic research has made the once harder challenge of statistically evaluating those events relatively easier.

Appendix

To potentially increase the power of the empirical test to estimate the covariances between the Italian stock market and each country’s CDS spreads on event and non-event days, the analysis assumes that each political event has three observations, that is, the day of the event and the days before and after that event. In this case each covariance matrix is estimated with 30 observations. Finally, the non-event day is a calendar week (7 days) distant from the political event.