Portfolio insurance proved all the rage during much of the 1980s. Equity market participants bought put options on the S&P 500 with the hopes of limiting their downside risk while still capturing most of the potential bull-market upside. The strategy’s fame quickly turned into infamy, however, when many market historians blamed some of the 1987 crash on portfolio insurance and automated trading.

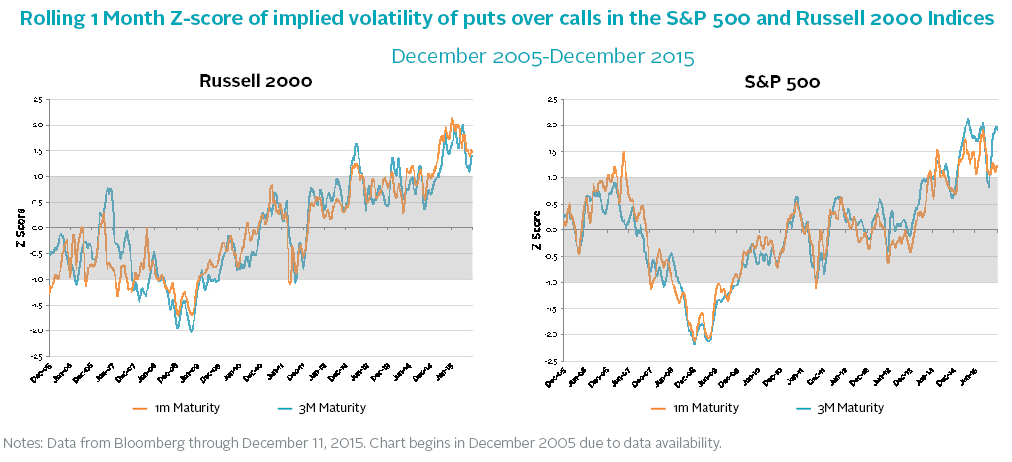

Today, portfolio insurance has become more expensive as investors and financial intermediaries like banks have more widely adopted the strategy. The relative skew of put versus call options on the S&P 500 index has sustained levels during past 18 months far higher than the ten-year average. At times, the skew has reached two standard deviations above the mean. On average, the skew exceeded 1.2 standard deviations. A qualitatively similar pattern exists for options on the Russell 2000 index.

What’s driving higher demand for portfolio insurance?

Multiple potential explanations exist. New regulations and assessments in the United States, including Dodd-Frank and the Comprehensive Capital Analysis and Review (CCAR), may have structurally changed the market by both forcing banks to better hedge their equity exposures and withdraw from their historical role as liquidity providers. For example, banks prepare for the Federal Reserve’s annual but increasingly important CCAR test by stockpiling put options to try to demonstrate that their equity positions could weather market stress.

More worryingly, equity market investors may feel apprehensive about the global economic outlook, inciting them to purchase greater amounts of portfolio insurance than during the recent past. Either way, the relative skew of put versus call options implies that the demand for portfolio insurance has increased relative to the supply.