As the impasse between the Syriza-led government and the country’s largest creditors continues to show no sign of resolution, Greece’s mostly on- but occasionally off-again debt crisis has once more reared its head.

In some ways, little has changed since Greece’s center-left PASOK party won power in October 2009 and revealed that Greece’s government deficit would exceed twelve percent of GDP. Greece still suffers from low or even negative growth, inefficient tax collection, and debt in excess of 175 percent of GDP and counting (IMF, 2015).

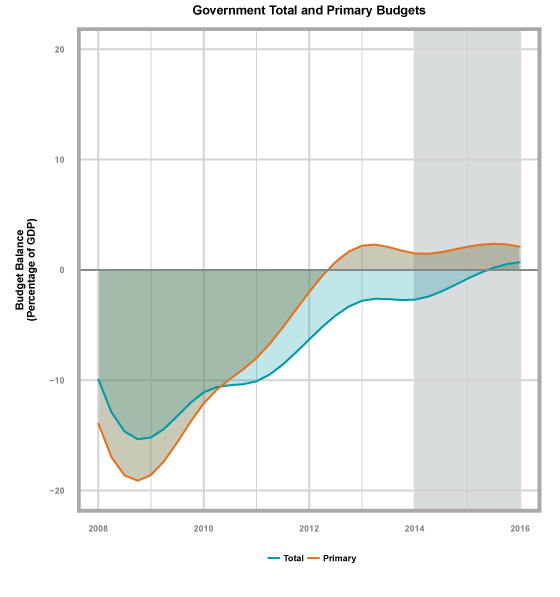

Some good news for Greece

In other ways, much has changed. The euro zone as a whole enjoys modest economic growth, and the financial stresses born by “periphery” countries (other than Greece) seem to have abated. Perhaps more importantly, Greece itself has made important reforms. It still runs a deficit of 2.7 percent of GDP, but its primary budget (i.e., its fiscal budget excluding interest payments) turned to a surplus in 2013.1

According to the IMF (see chart above), that surplus continued through 2014 and will likely persist for the next few years. So, even if Greece were to default – it faces nearly €6 billion in debt payments through July alone – the government could in many ways continue with business as usual, with the exception of paying creditors.