Institutional investors typically view Commodity Trading Advisors (CTAs) as an alternative investment that allows them to participate in multiple global markets as well as to better diversify and improve the risk-adjusted performance of their overall portfolio. Over the past few decades, that has generally proved true. The correlations between CTAs and equity and bond indices has historically fallen below 30 percent.¹

However, long-term averages may mask current risks. The recent, sharp fall in the SG CTA Index—a frequently used proxy for the CTA universe² —seems to have focused the minds of institutional investors on those risks. This performance, and the risk decomposition analysis below, highlights two important considerations for CTA investors:

1. CTAs may invest in numerous instruments and markets globally, but the CTA market seems to have only four major bets right now.

2. The average CTA’s current long exposure to both equities and bonds would seem to offer very little diversification for the typical institutional investor, making the asset class less “alternative” right now than some might hope.

Decomposing recent CTA performance

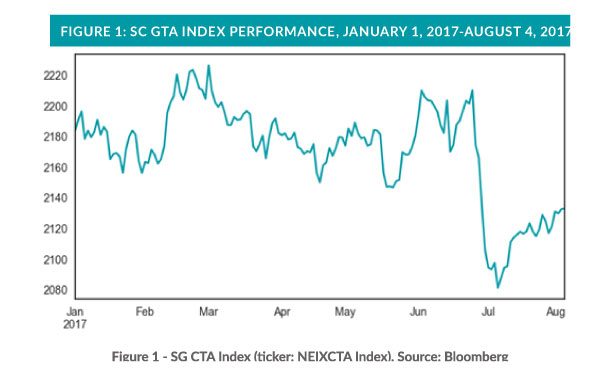

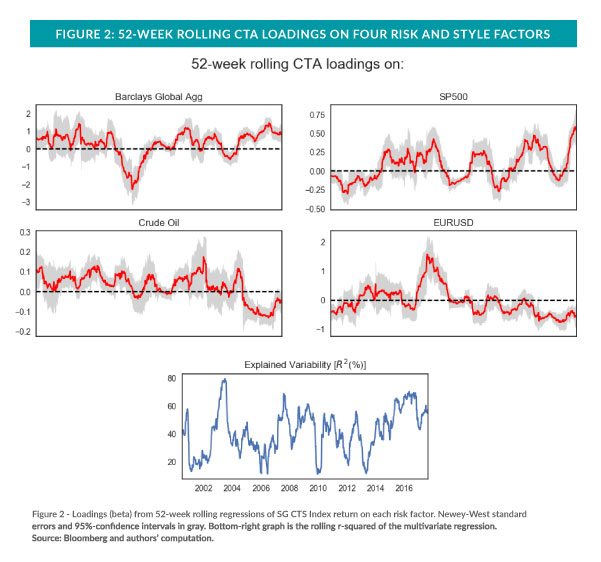

The SG CTA Index dropped sharply by about 4.36 percent the last week of June 2017. Although it soon recovered some of those losses, performance has remained negative year to date (Figure 1). A factor-based approach to analyze CTA performance may put some more color on the recent trend as it helps decompose it in the main driving risk factors. Four factors, representing the global fixed-income and U.S. stock markets, currency (EUR-USD), and crude oil collectively appears to explain about 60 percent of its weekly performance over the last year.³ During the last week of June and the first week of July, the simultaneous declines in US equity prices, global bond returns, and a weakening of the USD proved especially painful to CTAs.

This is not a short-term trend. As Figure 2 illustrates, index loadings over the past year show elevated long exposure to both the Barclays Capital Global Aggregate Bond Index and the S&P 500 Index—the latter measure being near its highest level of all time. Meanwhile, CTAs exhibit significant short exposure to the EUR-USD and to crude oil prices. The fraction of risk that these four factors appear to collectively explain has increased since 2015 and is the highest since the global financial crisis that started a decade ago.

Potential implications

Although the recent performance of the aggregated CTA market seems to point towards reduced diversification benefits for institutional investors, individual CTAs may have different exposures. However, asset allocators seeking diversification through CTA exposure cannot safely assume that such programs necessarily deliver uncorrelated returns at a given point in time. Institutional investors might find it more helpful to consistently and regularly conduct factor decompositions of their overall portfolio and their investment managers, instead of just relying on long-term trends.