The short-lived mini-“taper tantrum” that followed a recent speech by European Central Bank President Mario Draghi was only the latest instance of markets struggling to react efficiently to monetary policy news. Quantifying the effects of monetary policy shocks on asset prices remains a difficult undertaking, principally because such effects are not directly observable. Regardless, asset allocators routinely must not only handicap a policy shock’s probability of occurring, but also of its likely impacts on asset prices.

Academic research such as Rigobon (2003), highlighted in the December 2016 issue of Street View, provides a straightforward approach to modeling the effects of political risk on financial markets. This approach also proves useful in measuring the impact of monetary policy shocks on asset prices. With a meeting of the ECB’s Governing Council scheduled for July 20 and policy uncertainty likely to persist well beyond then, the Rigobon method may help provide guidance on likely market reactions should a surprise be in store.

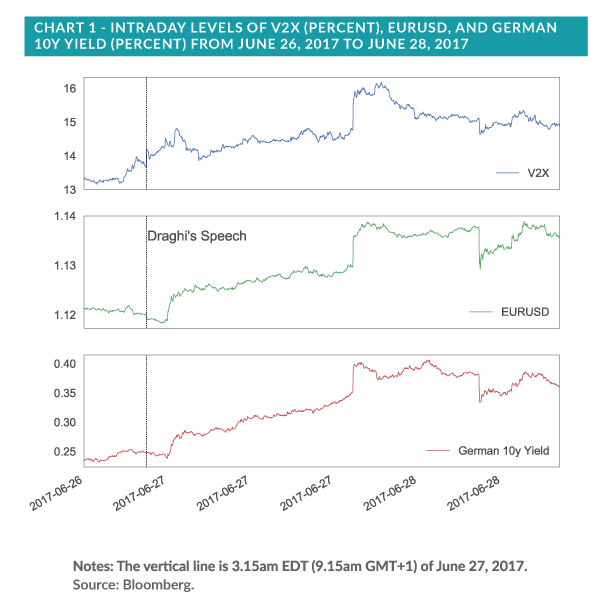

Markets reacted sharply to Draghi’s June 2017 speech

In what was likely meant to be a relatively un-newsworthy speech in Portugal on June 27, 2017, ECB president Mario Draghi briefly sent European markets reeling after noting that “deflationary forces have been replaced by reflationary ones.” Investors seemed to interpret the statement as a signal that the central bank aimed to tighten monetary policy soon, by starting to phase out its EUR60 billion monthly asset purchase program.

The market reaction was immediate, with 10- year German bund yields rising 15.5bps, the euro strengthening to its highest level against the dollar this year, and the EURO STOXX 50 Volatility Index (the European VIX, also known as the V2X) jumping 8.2 percent (Chart 1).

By the following day, ECB officials tried to clarify Draghi’s speech and suggested that the markets had misunderstood his level of optimism.¹ Asset prices soon stopped their euphoria. However, European equity and fixed income markets remain unsettled.

Quantifying policy uncertainty’s potential impact on asset prices

Monetary policy uncertainty is unobservable; as it mirrors the risk the market perceives about the central bank’s actions and consequences. However, Rigobon (2003) provides a methodology to potentially gauge the impact of unobservable risk factors on asset prices without directly quantifying it.²

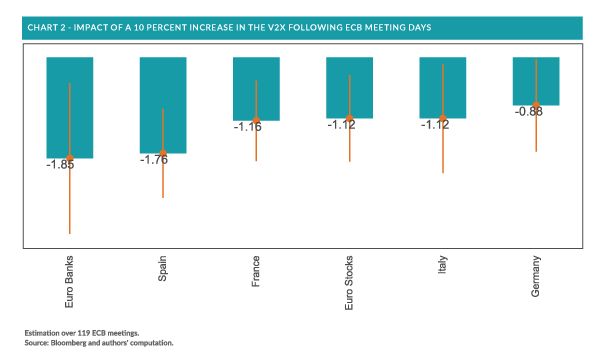

This approach quantifies the market impact by comparing the covariance between at least two variables on ECB meeting days to the covariance several days earlier. While it is impossible to identify the effect of uncertainty on both variables, Rigobon (2003) shows how to quantify the effect on one variable relative to the other. In this case, Chart 2 estimates the effect of uncertainty on equity markets relative to the volatility of the Euro Stoxx 50 (VSTOXX). The chart standardizes the results across instruments by normalizing VSTOXX changes to 10 percent on ECB meeting days.

As Chart 2 shows, a 10 percent increase in volatility would potentially have a large, negative effect on a range of equity indexes and subsectors, especially European bank stocks. Not surprisingly, the effect on German equities appears more muted than other countries. More interestingly, the magnitude of the difference (e.g., -0.88 for Germany and -1.12 for Italy) appears relatively small, suggesting that the dispersion in Eurozone economies has fallen since the peak crisis years.

Potential implications

The recent moves in the European stock and bond markets following Mario Draghi’s June speech suggest that monetary policy uncertainty remains one of the main sources of risk for investors with European equity exposure, at least in the short run. While the effects of policy shocks are not directly observable, an analysis of the historical evidence indicates that shocks have had a meaningful impact on European equity prices. Asset allocators may want to consider applying the Rigobon (2003) methodology when seeking to quantify their portfolio risks of monetary policy shocks going forward—especially if Eurozone economic data continue to improve and policy uncertainty persists.